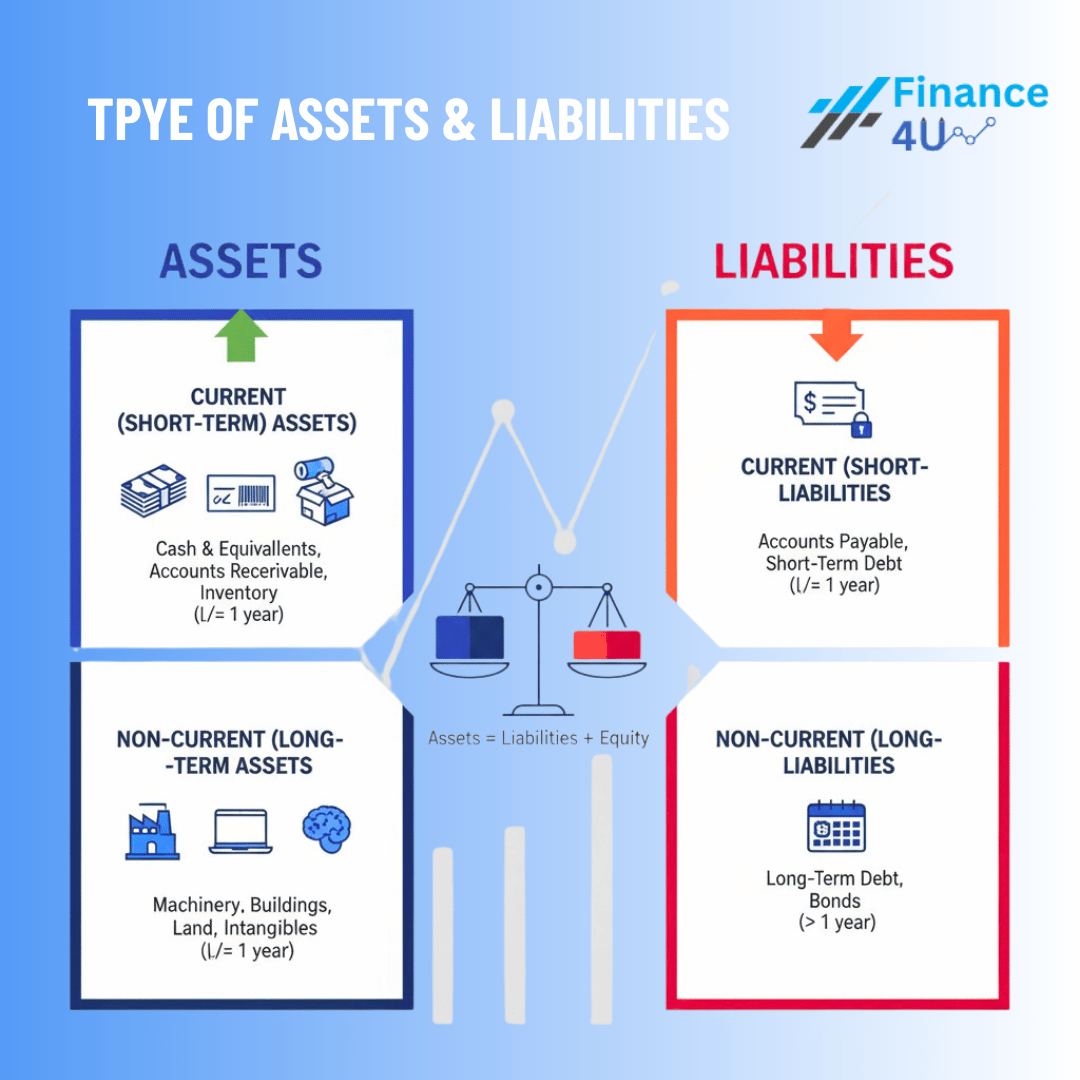

ប្រភេទទ្រព្យសកម្ម

ទ្រព្យសកម្មចរន្ត (រយៈពេលខ្លី)

ទ្រព្យសកម្មចរន្តមានអាយុកាលមួយឆ្នាំ ឬតិចជាងនេះ ដែលមានន័យថា ក្រុមហ៊ុនជាធម្មតានឹងទទួលបានអត្ថប្រយោជន៍ពីទ្រព្យសកម្មទាំងនេះក្នុងរយៈពេលមួយឆ្នាំ។ ឧទាហរណ៍ ក្រុមហ៊ុននឹងប្រមូលសាច់ប្រាក់ពីអតិថិជនក្នុងរយៈពេលតិចជាងមួយឆ្នាំ ដូច្នេះគណនីទទួល (accounts receivable) ជាធម្មតាជាទ្រព្យសកម្មចរន្ត។

ទ្រព្យសកម្មចរន្តរួមមាន សាច់ប្រាក់ និងសមមូលសាច់ប្រាក់ គណនីទទួល និងសារពើភណ្ឌ។

សាច់ប្រាក់ ដែលជាទ្រព្យសកម្មចរន្តដែលមានសភាពរាវបំផុត ក៏រួមបញ្ចូលទាំងគណនីធនាគារដែលមិនមានការរឹតបន្តឹង និងមូលប្បទានប័ត្រផងដែរ។ សមមូលសាច់ប្រាក់គឺជាទ្រព្យសកម្មដែលមានសុវត្ថិភាពខ្ពស់ដែលអាចបំប្លែងទៅជាសាច់ប្រាក់បានយ៉ាងងាយស្រួល។ មូលបត្របំណុលរតនាគារសហរដ្ឋអាមេរិក (U.S. Treasuries) គឺជាឧទាហរណ៍មួយក្នុងចំណោមនោះ។

គណនីទទួល (AR) មានចំនួនទឹកប្រាក់រយៈពេលខ្លីដែលជំពាក់ក្រុមហ៊ុនដោយអតិថិជនរបស់ខ្លួន។ ក្រុមហ៊ុនតែងតែលក់ផលិតផល ឬសេវាកម្មដល់អតិថិជនជាឥណទាន។ ចំនួនទឹកប្រាក់ទាំងនេះត្រូវបានរក្សាទុកនៅក្នុងគណនីទ្រព្យសកម្មចរន្តរហូតដល់អតិថិជនបានបង់។

ចុងក្រោយ សារពើភណ្ឌតំណាងឱ្យវត្ថុធាតុដើមរបស់ក្រុមហ៊ុន ទំនិញកំពុងផលិត និងទំនិញសម្រេច។ អាស្រ័យលើក្រុមហ៊ុន ការរៀបចំគណនីសារពើភណ្ឌនឹងខុសគ្នា។ ឧទាហរណ៍ ក្រុមហ៊ុនផលិតនឹងមានវត្ថុធាតុដើមមួយចំនួនធំ ខណៈដែលក្រុមហ៊ុនលក់រាយគ្មាន។ ការរៀបចំសារពើភណ្ឌរបស់ក្រុមហ៊ុនលក់រាយ ជាធម្មតាមានទំនិញដែលបានទិញពីក្រុមហ៊ុនផលិត និងអ្នកលក់ដុំ។

ទ្រព្យសកម្មមិនចរន្ត (រយៈពេលវែង)

ទ្រព្យសកម្មមិនចរន្តគឺជាកន្លែងដែលអត្ថប្រយោជន៍សេដ្ឋកិច្ចនឹងត្រូវបានដឹងក្នុងរយៈពេលលើសពីមួយឆ្នាំ។ ទ្រព្យសកម្មទាំងនេះមានអាយុកាលលើសពីមួយឆ្នាំ។ ពួកគេអាចសំដៅទៅលើទ្រព្យសកម្មរូបី ដូចជាគ្រឿងម៉ាស៊ីន កុំព្យូទ័រ អគារ និងដីធ្លី។ ទ្រព្យសកម្មមិនចរន្តក៏អាចជាទ្រព្យសកម្មអរូបីផងដែរ ដូចជាកេរ្តិ៍ឈ្មោះល្អ (goodwill) ប៉ាតង់ ឬសិទ្ធិថតចម្លង (copyrights)។

ការរំលោះត្រូវបានគណនា និងកាត់ចេញពីទ្រព្យសកម្មទាំងនេះភាគច្រើន ដែលតំណាងឱ្យថ្លៃដើមសេដ្ឋកិច្ចនៃទ្រព្យសកម្មក្នុងអំឡុងពេលអាយុកាលប្រើប្រាស់របស់វា។

ប្រភេទបំណុល

ម្ខាងទៀតនៃតារាងតុល្យការគឺជាបំណុល។ ទាំងនេះគឺជាកាតព្វកិច្ចហិរញ្ញវត្ថុដែលក្រុមហ៊ុនជំពាក់ភាគីខាងក្រៅ។ ដូចទ្រព្យសកម្មដែរ ពួកវាអាចជាបំណុលចរន្ត និងរយៈពេលវែង។

បំណុលចរន្ត (រយៈពេលខ្លី)

បំណុលចរន្តគឺជាបំណុលរបស់ក្រុមហ៊ុនដែលនឹងដល់កំណត់ ឬត្រូវបង់ក្នុងរយៈពេលមួយឆ្នាំ។ នេះរាប់បញ្ចូលទាំងការខ្ចីប្រាក់រយៈពេលខ្លី ដូចជាគណនីត្រូវបង់ (AP) ដែលជាវិក្កយបត្រ និងកាតព្វកិច្ចដែលក្រុមហ៊ុនជំពាក់ក្នុងរយៈពេល ១២ ខែបន្ទាប់ (ឧទាហរណ៍ ការទូទាត់សម្រាប់ការទិញដែលបានធ្វើឡើងជាឥណទានដល់អ្នកលក់)។

ផ្នែកចរន្តនៃការខ្ចីប្រាក់រយៈពេលវែង ដូចជាការទូទាត់ការប្រាក់ចុងក្រោយលើប្រាក់កម្ចីរយៈពេល ១០ ឆ្នាំ ក៏ត្រូវបានកត់ត្រាជាបំណុលចរន្តផងដែរ។

បំណុលមិនចរន្ត (រយៈពេលវែង)

បំណុលរយៈពេលវែងគឺជាបំណុល និងកាតព្វកិច្ចហិរញ្ញវត្ថុមិនមែនបំណុលផ្សេងទៀត ដែលដល់កំណត់បន្ទាប់ពីរយៈពេលយ៉ាងតិចមួយឆ្នាំគិតចាប់ពីកាលបរិច្ឆេទនៃតារាងតុល្យការ។ ឧទាហរណ៍ ក្រុមហ៊ុនអាចចេញមូលបត្របំណុលដែលនឹងដល់កំណត់ក្នុងរយៈពេលជាច្រើនឆ្នាំ។

Types of Assets

Current (Short-Term) Assets

Current assets have a lifespan of one year or less, meaning that the company will usually receive the benefit from these assets within a year. For example, the company will collect cash from customers in less than a year, and so accounts receivable is usually a current asset.

Current assets include cash and cash equivalents, accounts receivable, and inventory.

Cash, the most liquid current asset, also includes non-restricted bank accounts and checks. Cash equivalents are very safe assets that can be readily converted into cash; U.S. Treasuries are one such example.

Accounts receivables (AR) consist of the short-term amounts owed to the company by its clients. Companies often sell products or services to customers on credit; these amounts owing are held in the current assets account until they are paid by the clients.

Lastly, inventory represents the company's raw materials, work-in-progress goods, and finished goods. Depending on the company, the exact makeup of the inventory account will differ. For example, a manufacturing firm will carry a large number of raw materials, while a retail firm carries none. The makeup of a retailer's inventory typically consists of goods purchased from manufacturers and wholesalers.

Non-Current (Long-Term) Assets

Non-current assets are where the economic benefit will be realized over more than a year. These assets tend to have a lifespan of more than a year. They can refer to tangible assets, such as machinery, computers, buildings, and land. Non-current assets can also be intangible assets, such as goodwill, patents, or copyrights.

Depreciation is calculated and deducted from most of these assets, which represents the economic cost of the asset over its useful life.

Types of Liabilities

On the other side of the balance sheet are the liabilities. These are the financial obligations a company owes to outside parties. Like assets, they can be both current and long-term.

Current (Short-Term) Liabilities

Current liabilities are the company's liabilities that will come due, or must be paid, within one year. This includes both shorter-term borrowings, such as accounts payable (AP), which are the bills and obligations that a company owes over the next 12 months (e.g., payment for purchases made on credit to vendors).

The current portion of longer-term borrowing, such as the latest interest payment on a 10-year loan, is also recorded as a current liability.

Non-Current (Long-Term) Liabilities

Long-term liabilities are debts and other non-debt financial obligations, which are due after a period of at least one year from the date of the balance sheet. For instance, a company may issue bonds that mature in several years' time.

03/09/2025

Comments